- Andersons’ consultants are continuing to support their clients during the pandemic. If you require any advice, please contact your usual consultant, or the office on 01664 503200 or email [email protected].

- The UK Government has set challenging new targets for the reduction of greenhouse gases (GHG). This is likely to have implications for agriculture as one of the economic sectors that is seen both as part of the problem, and the solution, when it comes to battling climate change. The UK had a previous commitment to reduce emissions by 68% compared to 1990 figures by 2030. The target has now been extended to a 78% cut by 2035. The eventual aim is for the UK to be ‘net zero’ by 2050.

- New Regulations to protect water from pollution came into force in Wales from 1st April 2021. The rules, put the whole of Wales into a Nitrate Vulnerable Zone (NVZ). The Water Resources (Control of Agricultural Pollution) (Wales) Regulations 2021, apply to all land, but transitional periods have been provided for certain requirements where land was previously not within an NVZ. Full guidance can be found via https://gov.wales/sites/default/files/publications/2021-03/water-resources-control-of-agricultural-pollution-wales-regulations-2021-guidance-for-farmers-and-landmanagers.pdf

- The RPA has announced expiring Countryside Stewardship (CS) agreement holders may be offered a new five-year Agreement, instead of one-year extensions. So called ‘Mirror Agreements’ will be available for Mid and Higher Tier agreements which are due to expire on 31st December 2021. The new Mirror agreements will be offered under domestic CS regulations and subject to the 2022 manual. One-year CS extensions will no longer be offered.

- The RPA has given some updated information on Countryside Stewardship (CS) inspections, especially for agreements which commenced from 1st January 2021. CS (and Environmental Stewardship) agreements which started prior to this date must still meet EU rules for inspections. But for CS agreements starting on or after 1st January 2021 UK domestic rules apply and the RPA has changed ‘Inspection’ to ‘Environmental Outcome Site Visit’. In 2021 there will be two approaches to the ‘Environmental Outcome Site Visit’;

- Whole Agreement – will look at all the options in the agreement

- Campaign – this will just look at certain options which have been chosen for the year. For 2021, these are;

- Buffer Strips – SW1 and SW4

- Grassland Options – GS1, GS2, GS7 & GS17

- Boundary Options – BE3

- Defra has announced Organic Higher Level Stewardship (OHLS) agreements will now be eligible for one year extensions. Originally it had said extensions would not be available for Organic ELS/HLS agreement holders.

- The much-delayed consultation on the delinking of the BPS and lump-sum payments has been postponed again. It has now been put back due to the ‘purdah’ period ahead of the Local Elections. It will not appear before the 7th May.

- The International Grains Council (IGC) has released its first full supply and demand projection for the 2021/22 year. This shows 63mt more grain production than last year at 2,287mt (a 2.8% increase). But with consumption increasing by 54mt this only stops the decline in stock levels. The level of grain stocks entering the new marketing year is the lowest for four years – this is what is fueling the global price rises. The figures are marginal at this stage of the year, the current concerns over the dry weather, or the arrival of rain in the key grain growing areas of the world could have major swings in the availability of grains for the coming year, and prices.

- British Sugar believes total sugar production is likely to be just over 1mt in 2021; 10% higher than in 2020. The reason is a reversion to more normal yields after virus yellows disease caused a drop of 25% in crop output last year. The cold weather in February reduced aphid numbers which spread the disease. Crop plantings this spring are down 10% on the 2020 area of 103,000 Ha, but higher yields are expected to more than compensate for this.

- Commodity and farmgate milk prices remain good. The average Global Dairy Trade (GDT) index stood at $4,110 at the event held at the end of April. Closer to home, a further 1.4ppl increase in May for Arla member suppliers sees the co-operative leading the way on milk price. However, the cold, dry weather is continuing to curtail grass growth and production.

- Finished beef and lamb prices continue to exceed expectations. The deadweight beef price has passed the £4/kg price for the first time. And, after declining monthly since the middle of 2020, pig prices have started to increase.

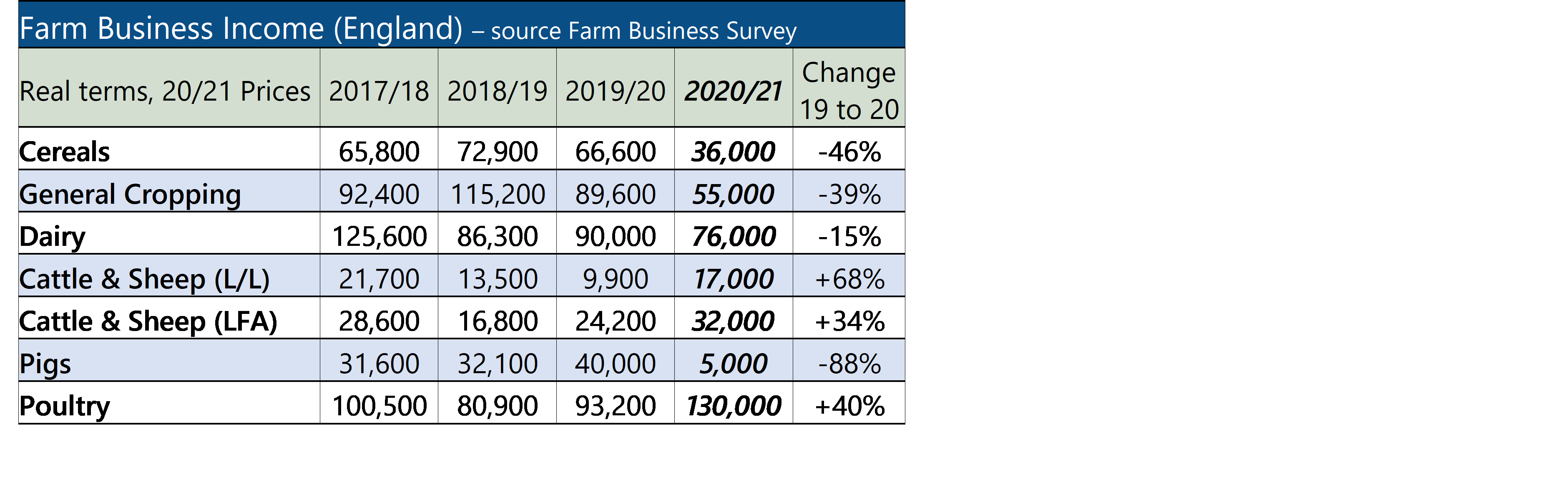

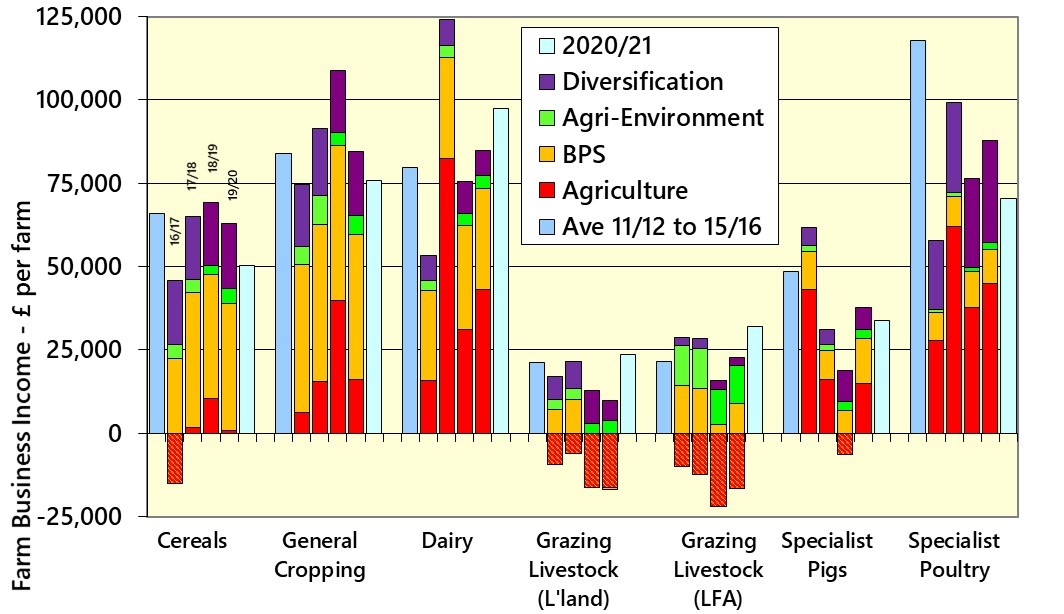

This month’s Spotlight looks at Farm Business Income, for England for the past year. Click Here for further information.

If you would like more detail on the topics covered above, why not subscribe to Andersons’ AgriBrief Bulletin? Over the course of each month, we give a concise and unbiased commentary on the key issues affecting business performance in the UK agri-food industry, and its implications for farming and food businesses. Please click on the link below for a 90-day free trial: