- Andersons’ consultants are continuing to support their clients during the pandemic. If you require any advice, please contact your usual consultant, or the office on 01664 503200 or email [email protected]

- The Chancellor has announced a further package of measures to support employment as the original ‘Furlough’ scheme is phased-out. A new Jobs Support Scheme (JSS) will top-up the wages of those who are working reduced hours, commencing on 1st November. The Self-Employed Income Support Scheme (SEISS) will also be extended for the period from November to the end of January to those eligible for the current SEISS. This will be reduced to 20% of average monthly profits, up to a total of £1,875. The temporary VAT cut for tourism and hospitality will be extended to the end of March. There will also be more time to pay deferred VAT payments, income tax, Bounce Back Loans and Coronavirus Business Interruption Loans. Full details are available at – https://www.gov.uk/government/news/chancellor-outlines-winter-economy-plan.

- It seems increasingly likely that the BPS in Wales will continue relatively unchanged for the next three years. With regards to other schemes, the Welsh Government has announced £106m worth of funding for the rural economy over the next three years. This will allow some of the current Rural Development Programme (RDP) schemes to open for new rounds. Dates for EOIs for a number schemes have been announced including;

- Farm Business Grant Scheme – 9th Nov-18th Dec 2020 & 18th May-25th June 2021, for yard coverings. 1st Mar-9th Apr 2021 for other items

- Sustainable Production Grant – 1st Feb-12th March 2021

- Glastir Small Grant Scheme – Carbon, 11th Jan-19th Feb; Landscape & Pollinators, 18th May-25th June 2021

- Controversy sparked in the UK-EU Brexit trade talks with the publication of the UK Internal Markets (UKIM) Bill as this would, by the UK Government’s own admission, break international law. There has been some signs of light, but the next month is crucial in the talks, as most commentators believe a Deal (or at least the outline of one) needs to be in place at the end of October, if it is to be ratified by the end of the Transition Period on 31st December

- The UK has secured an agreement ‘in principle’ with Japan; its first as a newly independent trading nation. However, it is unlikely to have a great effect on UK agriculture. Of far more importance are the ongoing talks with the USA, Australia and New Zealand. All of these are progressing, but no deal looks likely this year in any of them.

- Defra has announced the outdoor use of Metaldehyde will be banned in GB from the end of March 2022. The pesticide, which is used to control slugs on farms and in gardens was the subject of a ban announcement back in 2018, but this was subsequently overturned in the High Court.

- The AHDB estimates a British potato area of 119,000ha, down 1.0% on last year. Average yields would deliver a crop of 5.4mt; slightly more than the flood-impacted crop of last year. National yields are likely to be average at best. Prices have started the season on a weak note with little expectation for better returns later in coming months. The AHDB free-buy price is below £100 per tonne for the first time since the 2017/18 season. The market continues to be affected by Covid-19 restrictions.

- UK finished pig prices have been on a steady increase since March 2019, but the period of buoyancy may now be coming to an end. Falling prices across the EU are now influencing the British market. In addition, on 10th September Germany announced its first case of African Swine Fever (ASF). Germany is the largest European pork producer and exporter. But the spread of ASF into Germany may have less severe consequences on the market than it once would have had. Due to ASF in China, there has been a sharp rise in import demand and other countries in the EU have been sending significant quantities of pork to China, so that if Germany is unable to export and the volumes are retained in the EU, the market is unlikely to be swamped. Prices are still likely to decline, but probably not by as much as once feared.

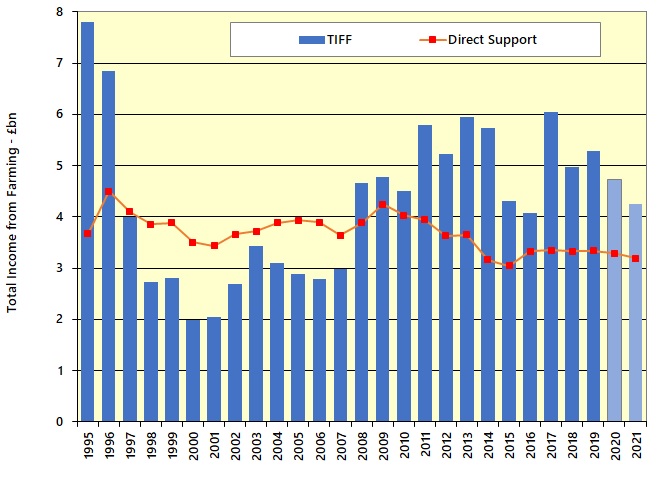

This month’s Spotlight gives an update on future agricultural support in England. Click Here for further information.

If you would like more detail on the topics covered above, why not subscribe to Andersons’ AgriBrief Bulletin? Over the course of each month, we give a concise and unbiased commentary on the key issues affecting business performance in the UK agri-food industry, and its implications for farming and food businesses. Please click on the link below for a 90-day free trial: