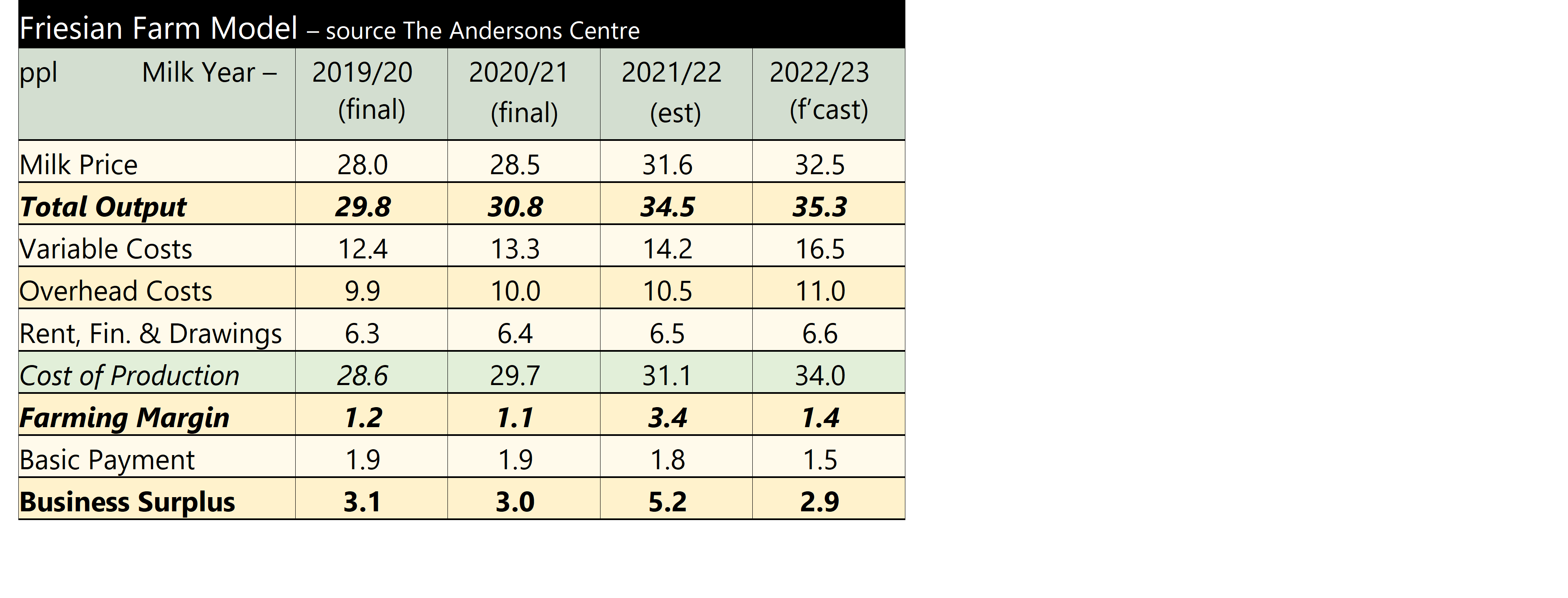

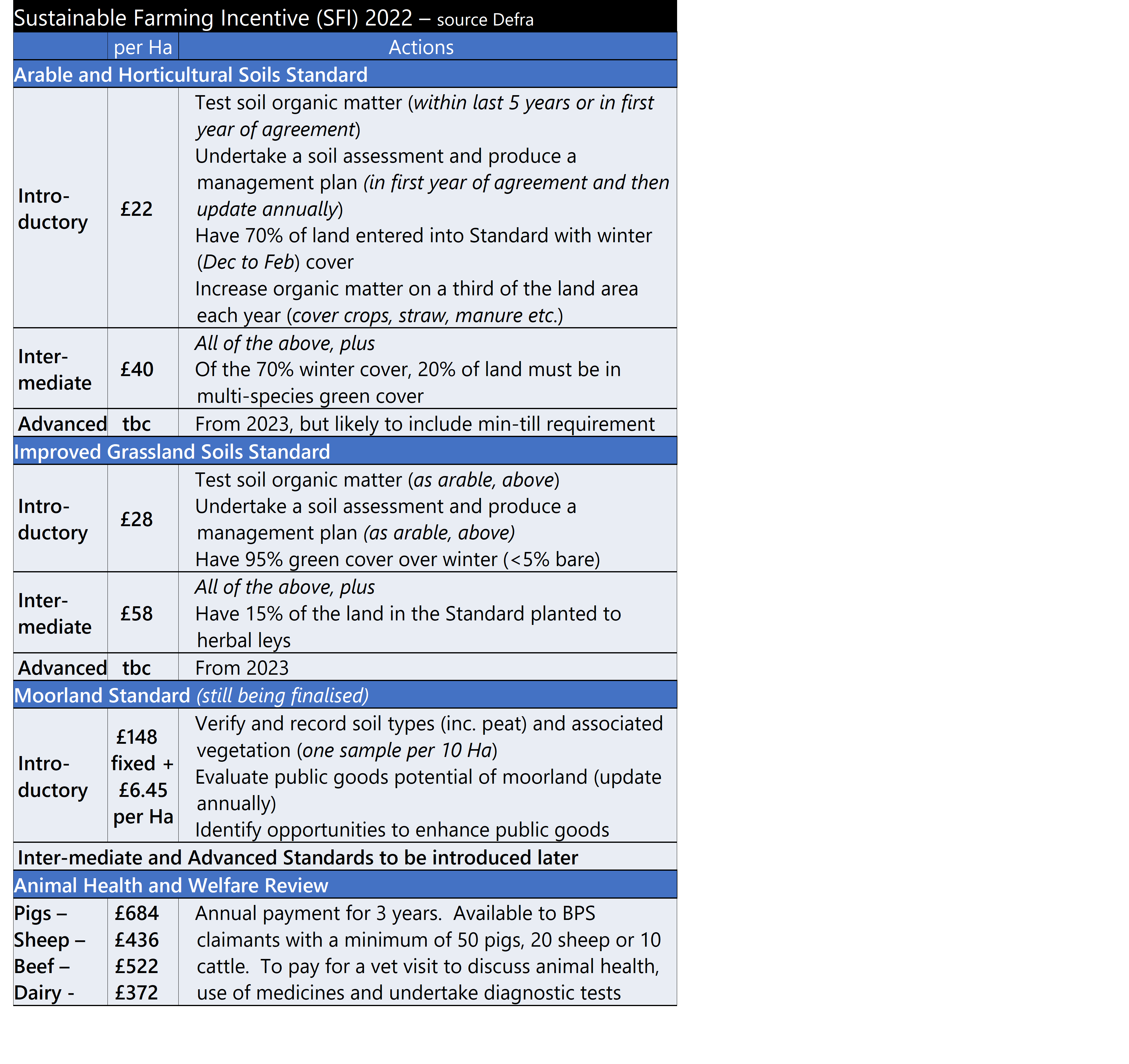

In the August 2022 edition of Farming Focus we take a look at the Sustainable Farming Incentive; if you are already in CS it’s not quite as straight forward to also have an SFI agreement. See how you can get a FREE farm business review. We report that most English farmers should have received their 50% advance BPS payment and if you are considering extending your HLS or CS agreement it could now be under (more favourable) UK rules. We take a look at the UK-Australia FTA and the latest farm profit figures for England. Finally, we inform Welsh readers of two new grants that are open.

Our Spotlight article this month looks at future farm policy in Wales after proposals for the new Sustainable Farming Scheme have been announced.

Click Here to access our August 2022 edition of Farming Focus.

If you require advice from one of our consultants, do not hesitate to contact them by email or phone. Their contact details can be obtained by clicking here. Alternatively, your can also contact our office on 01664 503200 or email [email protected]

If you would like more detail on the topics covered above as well as additional articles on UK farm business matters, why not subscribe to Andersons’ AgriBrief Bulletin? Over the course of each month, we give a concise and unbiased commentary on the key issues affecting business performance in the UK agri-food industry, and its implications for farming and food businesses. Please click on the link below for a 90-day free trial: