- If you require advice from one of our consultants, do not hesitate to contact them by email or phone. If you do not have their details please contact the office on 01664 503200 or email [email protected]

- The Lump Sum Exit Scheme is now open for applications. The Scheme is open until 30th September 2022 and is not expected to be available for applications in future years. It allows English farmers to take their future BPS payments through to 2027 in a single Lump Sum. In return, farmers will have to transfer out (rent, sell or surrender their tenancy) the agricultural land that was at their disposal on 17th May 2021. Up to 5 hectares of agricultural land can be retained, also any non-agricultural land and buildings including the farmhouse. The payment will be based on the average BPS payment received by the business for the three years 2019-2021 (the reference period). This will be capped at £42,500 and multiplied by 2.35, meaning the maximum payment will be just under £100,000. The full scheme guidance and application forms can be found via https://www.gov.uk/government/collections/lump-sum-exit-scheme. For further information please go to our article published in February.

- In response to rocketing prices of fertiliser, Defra has announced three measures to help farmers with their nutrient management.

- Urea: The planned ban on the use of urea fertiliser has been scrapped. Instead, an industry-run voluntary scheme will aim to reduce the ammonia emissions from solid urea fertiliser, commencing in 2023. This will be delivered through the Red Tractor farm assurance scheme and FACTS advisers.

- Farming Rules for Water: Defra has released ‘revised and improved’ statutory guidance on applying the Farming Rules for Water. The de facto ban on autumn manure spreading, based on how the rules were being enforced, has been removed. The Farming Rules for Water have not been amended. Instead, the new guidance tells the Environment Agency about criteria that they should consider when assessing if enforcement action should be taken under the regulations. It also provides some clarity for farmers as to how to manage the use of slurry and other manures during autumn and winter.

- Slurry Storage: The final Defra announcement was a confirmation that grants for slurry stores will be available in England. This will come under the Farming Investment Fund. Little detail is currently known, but grants between £25K and £250K at a 50% rate are expected to be available to fund up to 6 months of slurry storage. Stores will need to be covered and it may be possible to cover existing stores. The scheme is expected to be competitive. If you need any advice on increasing or updating your storage, please get in touch.

- The Welsh Government has announced it is making £227m of funding available over the next three years (2022-2024) to support Wales’ rural economy. This funding is in response to the ending of the EU Rural Development Programme (RDP), which will completely close in 2023. It will ensure continued support for the areas previously funded under the RDP such as environmental land management, capital equipment to improve productivity, nutrient management and on-farm storage. It will also provide support for organic farming and woodlands. Scheme details are still being drawn-up, but for 2022 £100m is being made available further details can be found at https://gov.wales/written-statement-funding-support-rural-economy-and-transition-sustainable-farming-scheme

- Field trials of a genetically modified barley have been approved by Defra. The study will use gene-editing techniques to investigate the role of existing barley plant genes that interact with soil microbes. The aim is to make the plants more efficient users of soil nutrients and reduce the need for artificial fertilisers. The trials will take place over the next 5- years at 3 sites of the Crop Science Centre; a partnership between the National Institute of Agricultural Botany and the University of Cambridge.

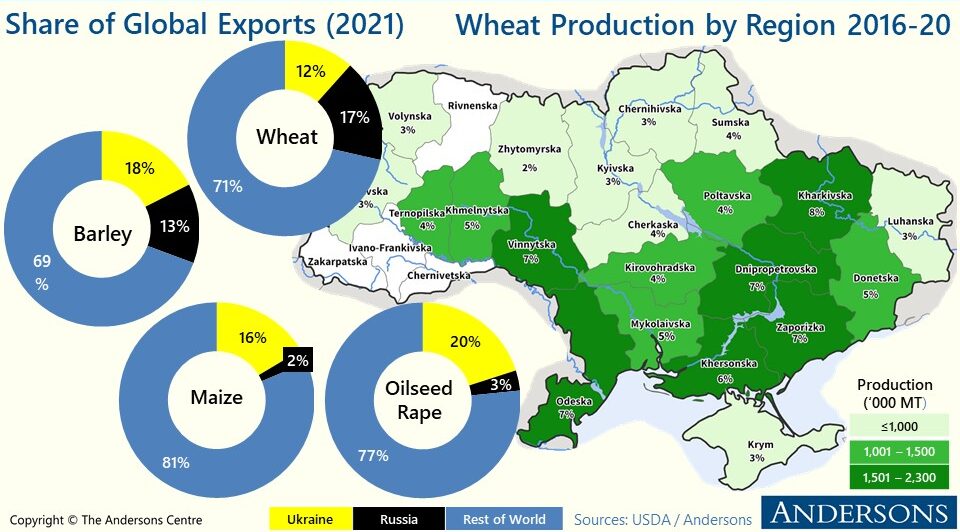

- The war in Ukraine has been the key driver of grain markets over the last two months and in the short-term it will continue to drive commodities and inputs. However, there are other factors also driving prices. Severe drought in parts of the US wheat belt has lowered US wheat crop condition ratings. In addition, the US maize crop is smaller as growers are opting for soyabeans over maize. The latest International Grains Council (IGC) supply and demand estimates, support the view of tight markets. World grain closing stocks are forecast to fall by 26.5 million tonnes from 2021/22 to 2022/23. But with the situation in Ukraine, all forecasts should be treated with caution.

- The Bank of England increased the Base Rate by a further 0.25% on the 5th of May. This takes the cost of borrowing from 0.75% to 1%. This is another attempt to respond to increasing inflation which is being exacerbated by the Russia-Ukraine conflict. The Bank is tasked with keeping inflation at 2% but, according to the Bank’s own forecast, increases in prices would rise above 10% this year. The rise in interest rates is meant to bring inflation back towards the target over the medium term. Many forecasters believe that there will be at least another 0.25% price rise before the end of 2022, taking rates to 1.25%.

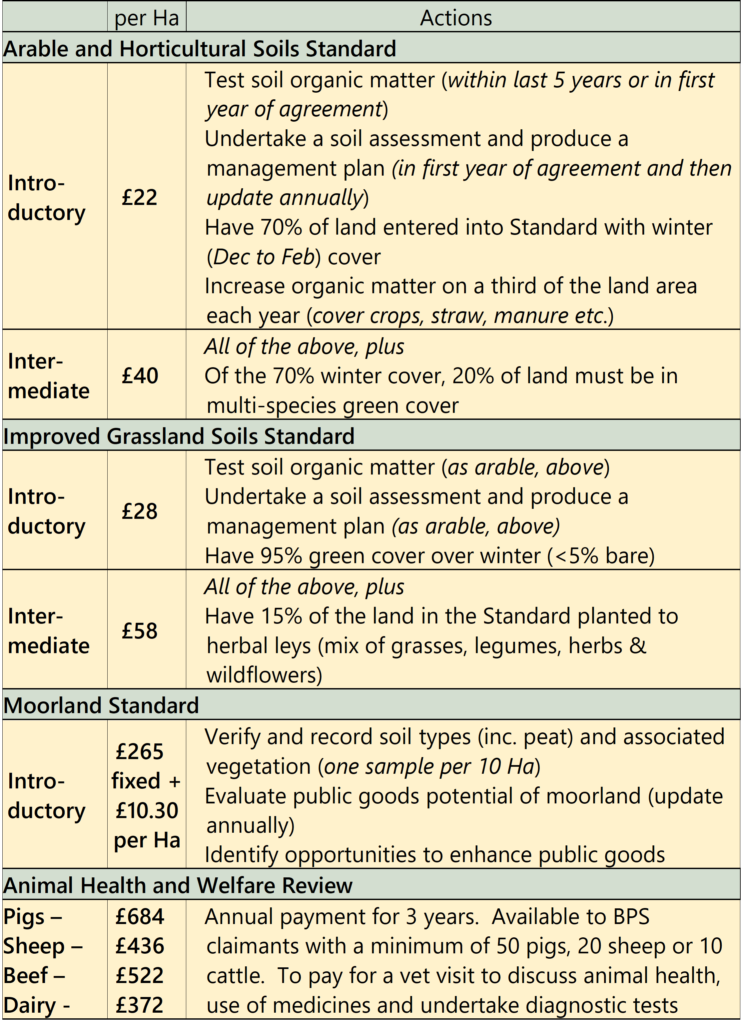

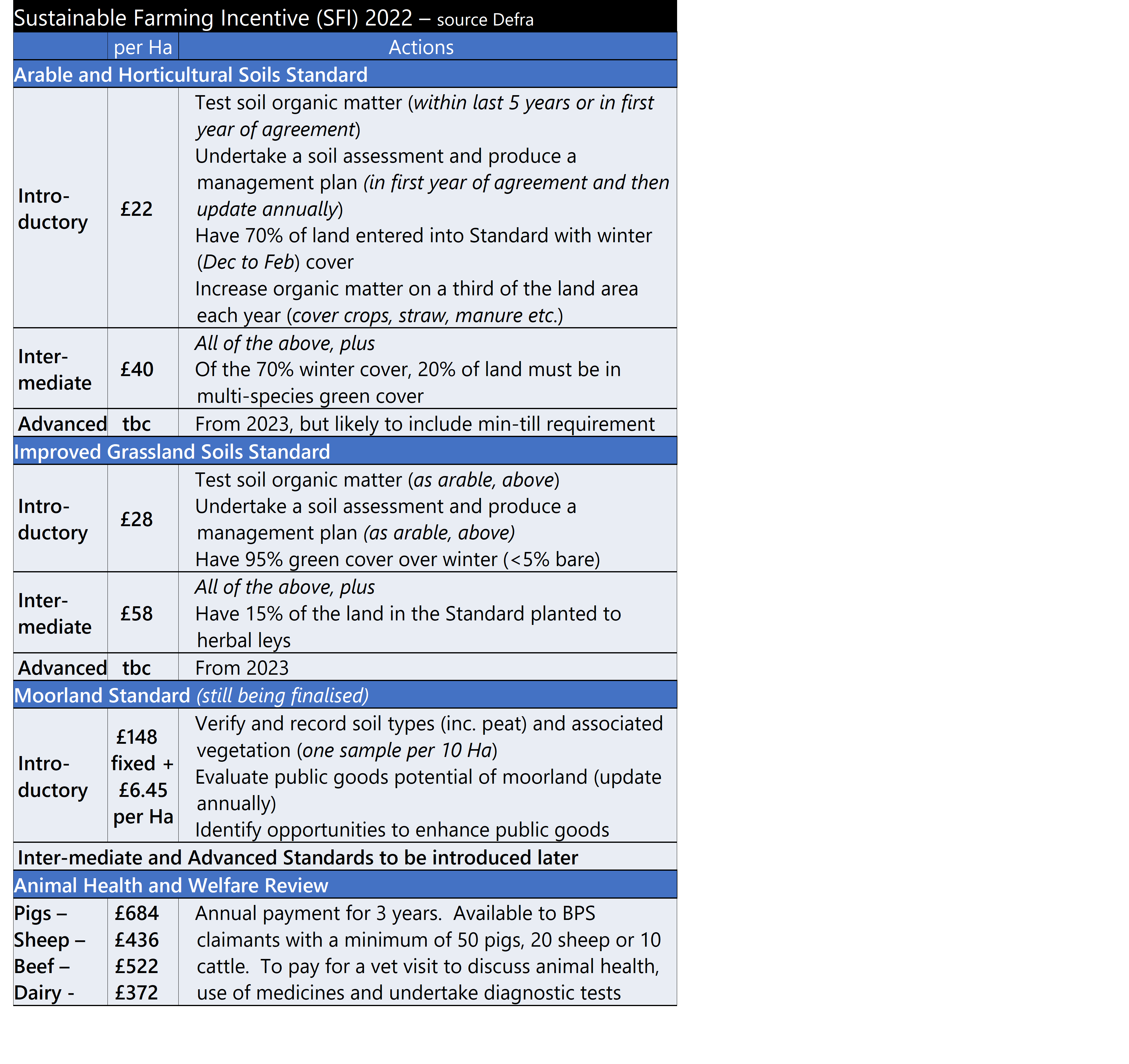

This month’s Spotlight looks at the recent Defra announcement on the Sustainable Farming Incentive (SFI). Click Here for further information.

If you would like more detail on the topics covered above as well as additional articles on UK farm business matters, why not subscribe to Andersons’ AgriBrief Bulletin? Over the course of each month, we give a concise and unbiased commentary on the key issues affecting business performance in the UK agri-food industry, and its implications for farming and food businesses. Please click on the link below for a 90-day free trial: